How Practical Are Livestream Shopping Applications for Whole Person Health & Wellness?

Last Fall, I wrote about synergistic opportunities that lie at the intersection of whole person health and large, proven adjacent markets such as consumer credit, embedded insurance and gaming. Since publishing that piece, it’s been awesome to see a handful of companies within that framework receive significant funding to catalyze their path forward (e.g., Ness, Spot, Hero Journey Club).

However, one intersection that I’m still curious to see play out is that of whole person health x livestream shopping. For those not familiar with our thesis, we define whole person health as being comprised of both upstream (i.e., consumer health & wellness and SDoH) and downstream (i.e., clinical) care.

While it’s easy to understand how consumer health & wellness brands within sexual wellness or sleep can effectively leverage livestream shopping for new forms of distribution, I’m also interested in exploring potential use cases for health care services as it relates to novel patient acquisition channels for DTC tech-enabled providers.

Before examining the pros and cons of a vertical livestream shopping platform for whole person health, let’s first break down the state of livestream shopping and analyze where it has found traction to date – both geographically and across specific verticals.

🎥 Livestream Shopping Background

Overview & Adoption

Livestream shopping is a form of social commerce that combines creator-led video demonstration of a featured product with instant purchasing and interactive audience participation.

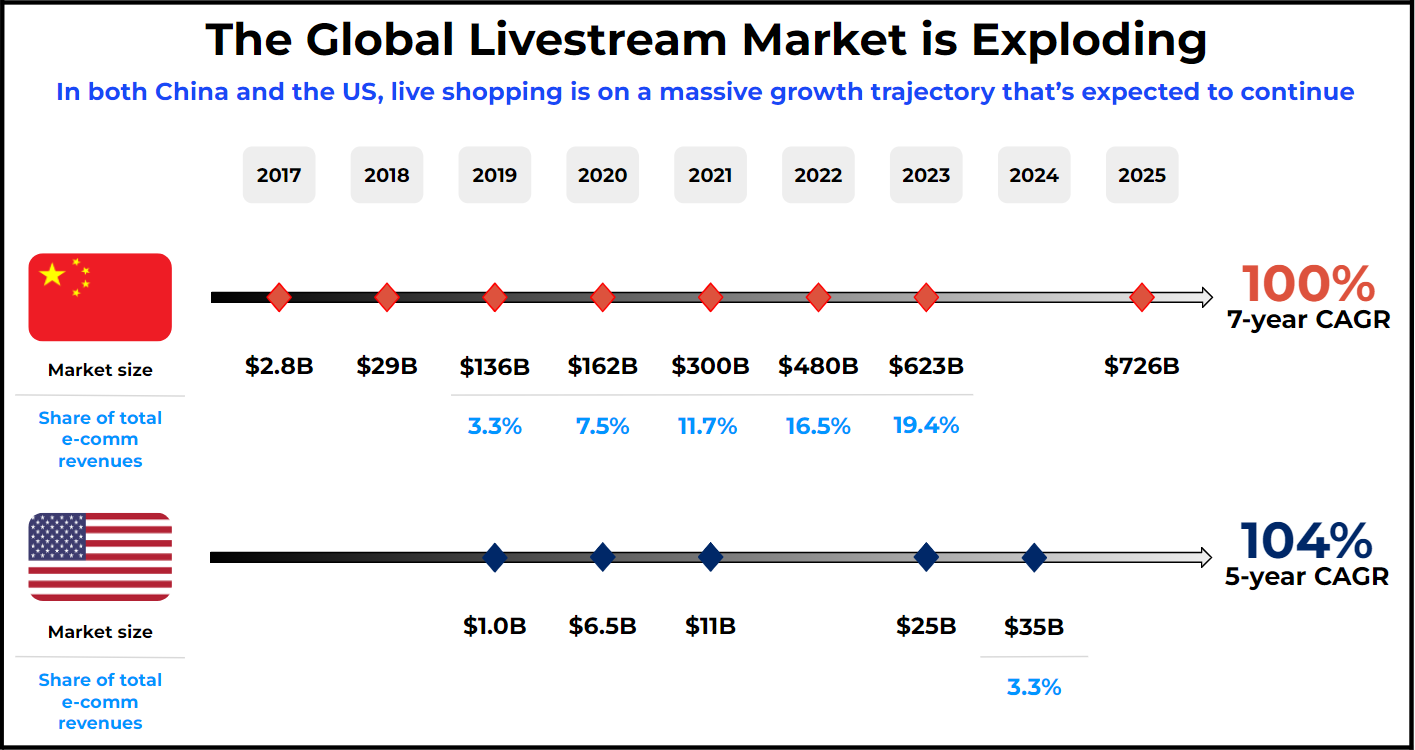

Livestream shopping has seen rapid adoption in China where it has become a cultural habit and is forecasted to eclipse over $500B in annual sales next year. While adoption in the US is finally gaining momentum through native vertical platforms, it’s taken much longer to materialize relative to China given societal differences in both consumer technology infrastructure and sociopolitical dispositions.

Adoption Disparity: Consumer Technology Infrastructure

The Chinese “Super App” ecosystem powers a frictionless end-to-end shopping experience in a way that the US app ecosystem is not designed to replicate.1 Consumers can move from discovery to checkout without ever leaving the platform, allowing for more effective awareness and cross-sell of social commerce features.

In comparison, the US’s ecommerce landscape remains fragmented. Large social networks provide effective product discovery, but migrate users to third-party sites with fourth-party payment processors to complete purchases, welcoming shopper drop-off.2 On the other hand, large ecommerce platforms like Amazon cater to customers with strong purchase intent, but suffer from a lack of product discovery. When’s the last time you proactively went to Amazon to browse their product catalogs?

This dynamic has resulted in a lack of funnel unification in the US, leading several big players such as TikTok and Facebook to shutter in-house livestream shopping initiatives given tepid consumer adoption.

Adoption Disparity: Sociopolitical Dispositions

As the team at RockWater conducted surveys and 1v1 interviews with several Chinese shoppers and platform execs, one stark cultural difference really stuck out to them – trust in central authority.

“Nearly 60% of respondents said TaoBao Live (owned by Alibaba) is their favorite platform. When we asked one active Chinese consumer why that is, she said ‘Because it’s owned by Jack Ma, who is the richest and most successful person in China, so I trust him’. Can you imagine any US shopper saying that about Jeff Bezos or Mark Zuckerberg?”3

This sociopolitical disposition creates a pervasive top-down mindset when it comes to influencing purchasing decisions of consumers, allowing top Chinese creators on large platforms to garner massive followings and to function as primary distribution points for a wide variety of products.

In contrast, Americans are inherently more autonomous and distrustful of central authority (i.e., capitalism vs. communism). The higher prevalence of individual sovereignty in the US has long driven consumer affinity for commercial aspects such as small business (e.g., mom-and-pop, local contractors, upscale boutiques). As the world evolves and digitizes, middle- and long-tail creators represent small business 2.0, taking market share and impressions away from large platforms as consumers turn to relatable creators on vertical platforms for product discovery and purchase.

🧱 Platform Types & The Importance of Supply-Side Curation

Using RockWater’s market framework, livestream shopping companies exist in two forms – Destination Platforms (i.e. B2C platforms) and Integrated Solution Providers (i.e., B2B infra). For this piece, I’ll focus on the former and its ability to effectively disseminate products and services across various verticals.

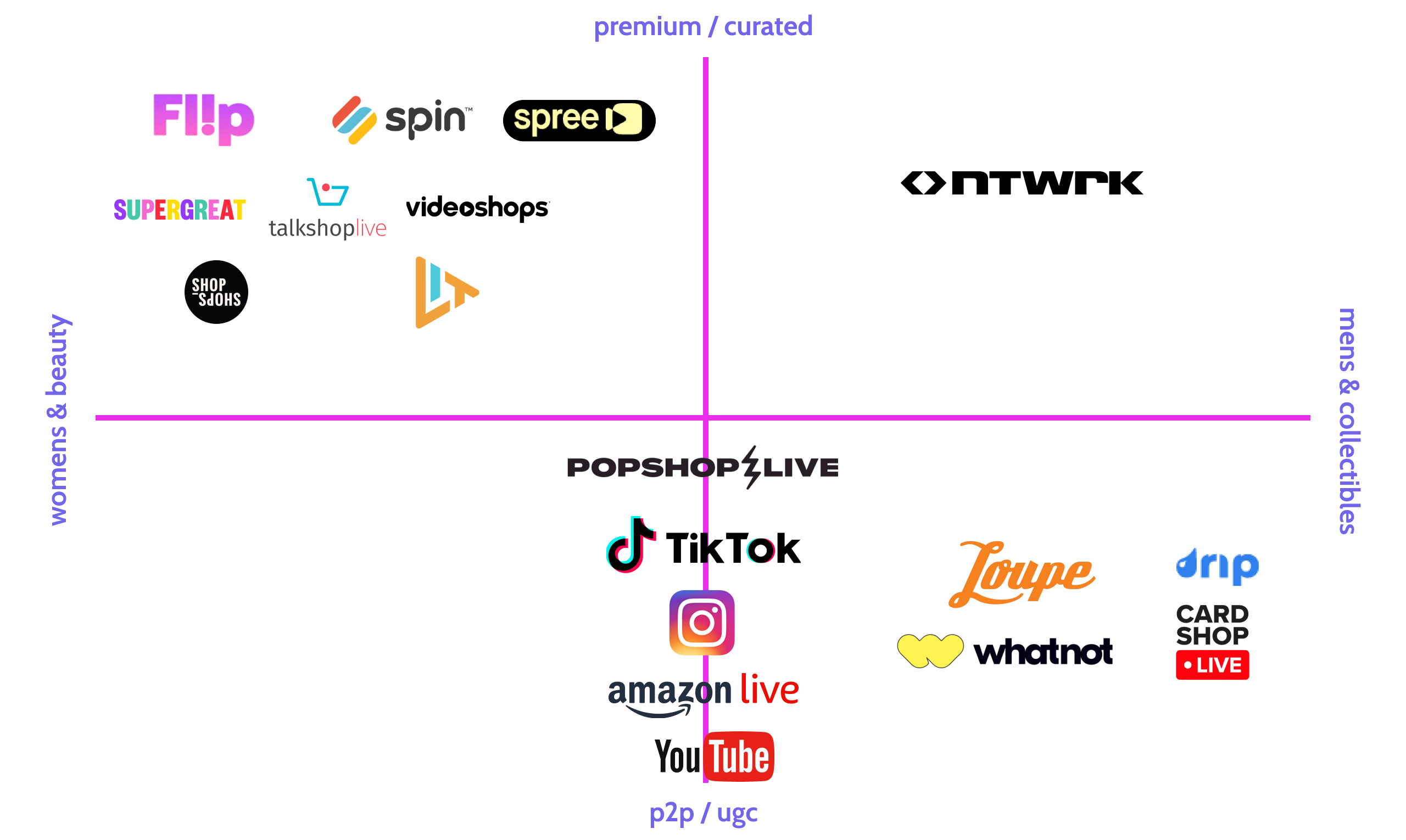

Destination Platforms are dedicated platform environments that consumers intently seek out.4 The universe of destination platforms is broken up into three distinct platform types – Content-first, Commerce-first, and Hybrid-native:

- Content-first: “Commerce-into-content.” Introduces social commerce features into incumbent social platforms. Examples include TikTok (via partnership) or Instagram layering on live shopping features to help creators and brands further monetize their content.

- Commerce-first: “Content-into-commerce.” Introduces content into incumbent ecommerce platforms. Examples include Amazon taking the fun and interactive nature of live video and using it as mid-funnel marketing to enlighten purchase consideration via Amazon Live.

- Hybrid-native: Rather than redefine the user experience of existing platforms, these new companies are content + commerce-native, building vertical livestream shopping experiences from the ground up. Examples include Whatnot, NTWRK and Flip.

Additionally, there are two supply-side frameworks that Destination Platforms can employ:

- Premium platforms: Prioritize quality over quantity. All of the content and streams featured by these platforms are programmed, planned, and produced by the platform itself, utilizing a curated group of creators. Examples include NTWRK, QVC and TalkShopLive.

- Self-service marketplaces: Decentralized, tech-enabled, UGC-driven ecosystems that provide independent sellers with “plug and play” tools and distribution to empower them to go live and sell to their communities whenever they want. Examples include Whatnot and Amazon Live.

Depending on the type of products or services being sold on the platform and the level of trust required around the sales narrative, supply-side framework matters greatly. I’ll get into this aspect more when we examine the importance of trust and reputation within whole person health.

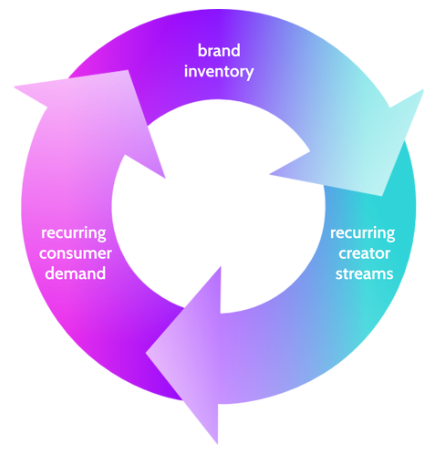

♽ Importance of Recurring Supply & Demand

In nascent markets like the US where the livestream shopping muscle has yet to be fully developed, the key to driving platform adoption is by sustaining recurring participation from both consumers and creators. Without both parties engaged, livestream shopping platforms fall apart.

Recurring Consumer Demand

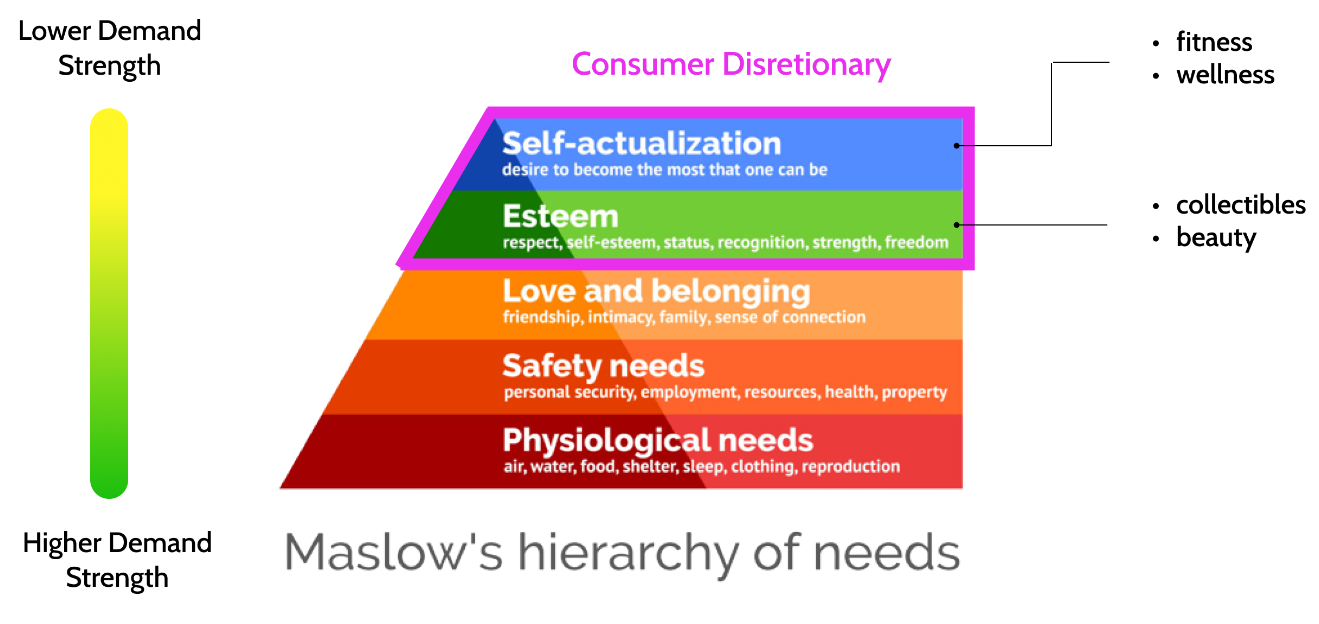

On the consumer demand side, not all verticals are created equal when it comes to (1) demand frequency and (2) demand strength, which is based on hierarchy of needs. Both components are necessary in order to sustain the demand side of any livestream shopping marketplace.

The collectibles space (e.g., sneakers, streetwear, trading cards) is a good example of a vertical that generates an outsized amount of demand frequency. Driven by rabid, hype-based demand for items with (intentionally) scarce supply, the collectibles space is predominantly made up of fanatical male consumers. These “hypebeasts” are always looking for the next drop to scratch their never-ending itch for social status.

It’s worth noting that the scarcity component of these products also makes consumers more prone to impulsive purchasing, which is a key characteristic that livestream shopping thrives at exploiting through features like exploding auctions and platform exclusive promos.

Ultimately, these unique consumer traits come together to drive strong demand frequency (i.e., increased transactions and CLTV) and a high density of DAUs.

In terms of demand strength, it should be no surprise that consumer discretionary verticals that directly appeal to Esteem needs (i.e., status, recognition) are stronger motivators of demand than those appealing to Self Actualization (i.e., proactive growth), per Maslow’s hierarchy of needs.

As such, Esteem-based verticals are functioning as the beachhead for driving livestream shopping adoption in the US.

Recurring Creator Supply

Recurring consumer demand within verticalized livestream shopping experiences cannot exist without equal (or greater) recurring creator supply.

Top Chinese creators are able to churn out daily streams because they always have cool new products to offer via hundreds of thousands of brands who want access to their massive viewership. Certain brand partnerships even allow creators to delight their fans by offering discounted or exclusive access to products. On average, top Chinese creators feature about 80 different products over the span of a four hour stream!5

In the US, top creators have historically only participated in livestream shopping for infrequent tentpole events, causing consumers to do the same.6 As a result, the lack of recurring content creation has deterred brands from fully exploring livestream shopping platform partnerships given the opportunity cost of impressions across other larger, proven channels.

Ultimately, a lack of brand buy-in results in lower levels of inventory/SKUs made available to creators and lower stream frequency. The team at RockWater calls this supply-side issue the “product gap”. In order for a creator to go live on a recurring basis, they need a recurring stream of fresh products that they can authentically and enthusiastically endorse.7

We’re now starting to see hybrid-native platforms reduce the product gap in various ways. For example, Whatnot employs a self-service marketplace model (i.e., UGC) that taps into the expansive long tail of hypebeasts and collectors who are interested in monetizing their rare inventory. Alternatively, Flip employs a premium marketplace model in which its curated set of creators access a rapidly growing list of beauty brand partnerships. According to TechCrunch, Flip is now signing an average of 20 new brands per week and has already secured partnerships with Unilever.

🏃🏾♀️⚕️ Whole Person Health Applications

As increasingly health-conscious, emerging generations age up, companies are rapidly mobilizing to meet their needs. As a result, there is an increasing number of products and services in both upstream and downstream care that are suffering from market saturation.

For example, in consumer health & wellness, consumers struggle to differentiate across relatively commoditized products within nutrition or beauty – a paradigm that has only been exacerbated by the explosion of DTC over the past decade. Additionally, as companies try to counter market saturation with net new innovation, nascent hardware products like CGMs or at-home blood diagnostic devices often come with daunting implementation experiences that affect consumer propensity to purchase.

In health care services, the explosion of digital health has spawned a number of DTC tech-enabled providers across primary and specialty care. Behavioral health is one specialty care example that has suffered from an uptick in CACs due to increased competition. For instance, when assessing provider options, the difference between services such as TalkSpace, BetterHelp or any other emerging provider is nebulous. While patient choice is sadly often dictated by provider availability given the disparity in provider supply and patient demand, it’s still extremely difficult for patients to understand how one provider care model may differ from another without existing patient testimonials and reported outcomes.

These pain points across whole person health make purchase and/or care decisions difficult for consumers and acquisition costs expensive for brands and providers. The latter group must abstract away commoditization in their marketing narrative, which is a difficult task to do via short-form video disseminated through paid and organic social.

The reason I’m so keen on assessing the viability of livestream shopping for whole person health products and services is that I believe health is a vertical in which highly engaging, live demonstration can have a disproportionate value on conversion, providing a new distribution channel for brands and providers.

Think QVC 2.0 in which verified, health-focused creators are leveraged to demonstrate the USP and/or utilization of consumer health & wellness products or to evangelize the patient experience of various DTC tech-enabled providers.

That said, there are significant risks inherent to health that would threaten the viability of a livestream shopping platform purpose-built for the space. Let’s examine these risks through the lens of the aforementioned supply-side and recurring demand frameworks, distilling out the pros and cons of each.

Pros and Cons: Supply-Side Framework

Trust is the essential factor needed in order to build a successful verticalized social commerce platform focused on health. This is especially relevant given the recent bout of bad actors on TikTok who are incorrectly influencing wellness or medical decisions through engagement juicing techniques such as “science washing” or abusing the platform’s powerful targeting algorithm to push medication (e.g. Adderall) onto people who don’t have a qualifying condition just to increase profits. As such, the choice of supply-side framework is vitally important.

If a platform leverages a premium marketplace design in which the creators are curated to prioritize validity (e.g., certified nutritionists, certified trainers or medical professionals), both the user experience and conversion rate are augmented by trust.

On the other hand, employing a self-service marketplace that allows anyone to make unverified claims about how to approach upstream or downstream aspects of one’s health is a one-way ticket to disaster.

It’s important to note that the solicitation of health care services through either supply-side framework faces additional risks around HIPAA compliance or malpractice if any message gets construed as a diagnosis.

Pros and Cons: Recurring Demand Framework

Hybrid native platforms in the US have found success by starting in one sub-vertical with cult-like demand and expanding horizontally thereafter. For example, Whatnot first focused on being the go-to trusted spot for buying and selling authenticated Funko Pop figurines. Once the company achieved that status, it slowly expanded to related niches like trading cards and sneakers to ultimately become “the” livestream shopping destination for collectibles.

Within whole person health, consumer health & wellness represents a good starting point given the higher liquidity of products in the space relative to health care services and the fact that it’s much easier to demonstrate value for a physical product than a service.

However, choosing a few sub-verticals to anchor on within consumer health & wellness is important as they must consist of products that can generate adequate demand frequency and strength.

Sub-verticals like sexual wellness or sleep first come to mind over ones like fitness, which is fully rooted in self actualization. I question the ability for self actualizing products to effectively generate sufficient demand strength given consumers generally have a lower willingness to pay for products whose primary benefits are realized further out into the future – also known as cognitive discounting. I shared a similar concern around this concept in my last piece and how it can negatively impact GTM scale.

When thinking about horizontal expansion options, further misalignment exists within selling digital health care services. Both primary care and specialty care come with their own unique challenges as it relates to the ability to generate recurring demand.

Given that primary care is more preventive in nature, utilization similarly suffers from cognitive discounting and a lower willingness to pay. On the other hand, while specialty care patients have a high willingness to pay for the treatment of chronic conditions, they are longitudinal in nature (i.e., no patient wants to swap specialty providers multiple times). In other words, neither care type is well suited for cultivating daily- or weekly-active consumers with high demand strength.

Final Thoughts

Despite my theoretical enthusiasm for a livestream shopping platform purpose-built for whole person health, I candidly struggle to have practical conviction around the approach. This view is mostly driven by highlighted concerns around platform trust/ethics and skepticism around whether the majority of health & wellness products can sufficiently generate both demand frequency and strength at scale.

I don’t doubt the ability for health & wellness to represent a feasible expansion area for platforms that have found initial fit within beauty, for example, but I do have concerns about a standalone livestream platform focused on the space.

The other side of the argument says that the health & wellness market is much larger than verticals like collectibles and that demand frequency and strength will only increase as emerging generations allocate more share of wallet than ever before on health & wellness products.

The US livestream shopping market is still so nascent and I wouldn’t be surprised to see market consolidation in which one leading platform rolls up multiple vertical platforms instead of having said multiple platforms operate in a standalone fashion.

I’d love to hear viewpoints on whether folks see viability for a standalone platform and what sub-verticals (e.g., sleep, sexual wellness) are best suited for this distribution channel.

If you are building or investing in the healthcare or health & wellness space, I’d love to chat! Please reach out to jordan@nextventures.com, or I can be found here.

To talk to the RockWater team, ping us here.